Is It Worth Investing In IPO's?

- Jun 11

- 5 min read

Some weeks, it can be a wee bit of a challenge to come up with something to write about.

This is not one of those weeks.

If the word on the street is to be believed, Space X will begin trading on the stock exchange tomorrow. At a slated price of $135 a share the offering seeks to raise a casual $75 billion - smashing the previous record for an Initial Public Offering (IPO).

This $75 billion will be in exchange for just 4% of Space X - give or take. If the shares are floated at $135 a piece, it would value the company at around $1.75 trillion.

Huge, mind blowing numbers. But let’s rewind for a sec.

What is an IPO?

An “initial public offering” is when a private company sells shares to the public for the first time, listing on a stock exchange so normal Joes like you and I can buy and sell them.

Before an IPO, ownership of the company is restricted to founders, employees, and private investors. After it, the company is “public” and anyone can own a piece. SpaceX has been privately held since 2002, tomorrow will be the first time the shares trade on the stock market as we all think of it.

Companies choose to “float” on public exchanges for two reasons: to raise capital, and to let early backers and employees cash out.

When a company decides to have an IPO they will hire investment banks to value it, set an offer price and line up buyers for the shares.

On listing day those shares start trading, with the hope that the shares go up (or “pop”) on day one so the early backers can get out at a nice price.

Why Now?

When companies list on a public exchange they want to see their shares go up, that much is obvious. So it makes sense to float in a strong market environment.

During a rough year for stocks in 2022, IPO activity fell off a cliff - only rebounding back to “normal” levels in 2025.

So far 2026 has been a great year for equity investors. And so it is probably no surprise that we are now seeing huge fund raises - not just from Space X, but if reports are to be believe Anthropic (Claude) and Open AI (Chat GPT) are looking to list this year as well. These would be monster issuances.

Already established companies are also choosing to raise money from investors at this point in the cycle too - Google announced last week they had raised $80 billion in a private placement to fund the building of AI compute infrastructure (this is a consistent theme at the moment).

All this money has to come from somewhere. Just taking Space X alone, $75 billion is a huge amount of supply for the market to absorb.

Just the amount that Space X are raising is enough to buy AirBnB in its entirety and have some change left over. It is approximately the same amount of money that we in the UK spend on defence each year.

Slapping a total valuation of $1.75 trillion on Space X would make it, overnight, the eighth biggest company on the planet. Bigger than Tesla, bigger than Meta.

Sharper minds than mine have looked at whether such a valuation is justified. Executive summary - it can’t be based on its current performance.

The company doesn’t currently make a profit, but this doesn’t mean the share price can’t go up. By investing in Space X you aren’t buying today’s reality, you are investing in the promise of a pipedream.

Put another way, at this stage whether the share price goes up or not depends entirely on vibes, not valuation.

How have investors in IPO’s done historically?

Research consistently demonstrates that while IPOs usually experience a share price “pop” on their first day of trading - longer term most IPOs go on to underperform the broad market.

Jay Ritter is the “go to” academic on the performance of IPO’s. His study of 1,497 public listings from 2012 to 2021 showed that on average IPO’s underperformed the broad market by an average of 21.6% over three years.

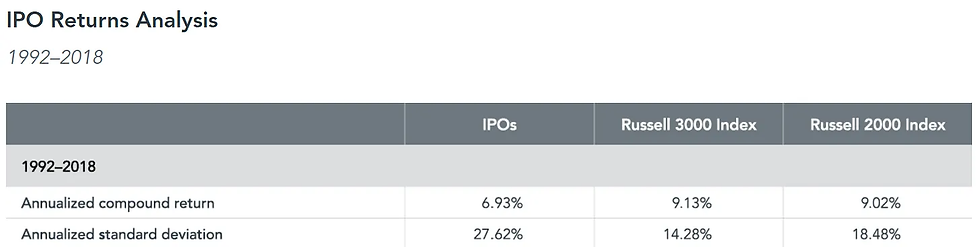

Our chums at Dimensional had similar findings. From 1992 to 2018, a basket of Initial Public Offerings both materially underperformed the Russell small and mid cap indices, and experienced higher volatility into the bargain.

Now, the reason this last study is particularly interesting is because Nasdaq have bent over backwards to get Space X to list on their exchange.

In what I am sure is a total coincidence, Nasdaq have recently announced that they will allow certain companies to “fast track” inclusion into the Nasdaq 100 index after listing. Until very recently it would take a minimum of three months before a stock was included within this index, to allow the share price to settle down post float. Now, a company can be included after only 15 days.

This is important because there are hundreds of billions of dollars in index funds tracking the Nasdaq indices. None of which can be used to buy Space X shares without Nasdaq first including it in their index.

So far S&P, who provide the other main indices in America are not changing their rules to get SpaceX into the indices faster. It will take at least a year post-listing before the stock is included within the S&P 500.

Does any of this matter to me if I just by index funds?

On the surface, no not really. But it depends on what index you are buying.

The below estimates depend greatly on the performance of the stock before its inclusion within the relevant index - so the numbers will invariably be a bit out. But you’ll understand what I’m getting at.

So to the properly diversified investor, Space X is a rounding error. The MSCI All Country World Index is a properly diversified global index and Space X is just immaterial. If the stock gets cut in half no-one will notice.

The more existential problem for those of us invested in the global markets as a whole, is what happens if the cumulative effect of all of these listings means that supply overwhelms demand.

As I mentioned above the money to support these listings needs to come from somewhere, and that somewhere is likely to be other stocks.

In the short term, all that really drives share prices is the balance between buyers and sellers. If there are more sellers than buyers, prices fall.

And maybe that’s what happens here. Maybe supply overwhelms demand to the point that markets correct. Maybe investors find the money down the back of the sofa and the party continues. We’ll have to wait and see.

Overall, you still only have one job really. Always be ready for a pullback, so you aren’t surprised when one comes.

Past performance is not indicative of future returns. None of the above is intended to represent investment advice to any individual. If you have any questions about your specific situation, feel free to drop me a line at david@beechgrovefinancialplanning.co.uk or consult with another regulated financial adviser.

Comments