The Gamblers' Fallacy

- Jan 1

- 3 min read

The scores on the doors are in, and it was a good year for investors.

The global stock market (as defined by the MSCI All Country World Index) returned 13.9% last year, which is pretty good. Better when we consider that this also comes on the back of strong returns in 2023 (up 15.3%) and 2024 (up 19.6%).

So that has been three great years in a row.

Now, given that historically equity markets have generated positive returns during calendar year periods around three quarters of the time, the temptation is to conclude that we are due a bad ‘un.

You may be surprised to hear, but I do actually think we are due a more difficult year. That market valuations could do with digesting some of the AI-powered earnings growth that is being factored into prices today.

But I am doing absolutely nothing tangible based on this.

There are a couple of reasons why - clients’ money (along with my own) deserves better than being managed based on a hunch. I am often wrong, and no doubt probably will be again here.

Secondly, and more importantly, the data tells us that there is no correlation between stock market returns one year and the next.

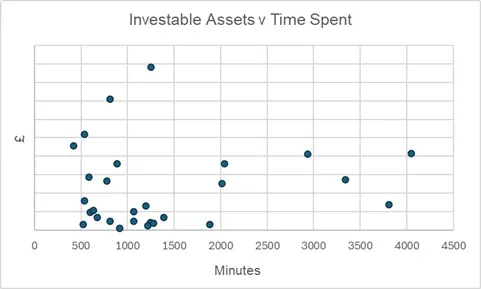

The below chart shows calendar year returns for the MSCI World Index from 1976 to 2024 on the x-axis, plotted against the return for the following year on the y-axis.

If you can find a pattern in the above, then well done you because I can’t. Looks like a shotgun spray.

Bad years do not seem to reliably predict good years, nor vice versa. Stock market performance year to year seems to be inherently random, other than the fact of course that most years are good years.

Putting it another way, just because I flip a coin three times and it comes up “heads” each time does not mean that “tails” is any more likely on the fourth go. To conclude so would be fallacy, the “gamblers’ fallacy” to be specific.

We all have our hunches, and we can’t go through our investing lives as robots. Of course we are going to have our own view and expectation of what is coming down the pipe. These views may even be incredibly well informed.

But we must also remember the bar for acting is a hell of a lot higher than the bar for thinking. Before we take real life action with our investment portfolios we must think very long and very hard - for activity and returns are not, traditionally, natural bedfellows.

I said I’ve not been doing anything based on my hunches and that is admittedly a bit of a fib. We’ve been undertaking our usual stress testing of financial plans, and will be reviewing cash allocations as part of our usual Q1 check ins with clients.

It also makes sense to prep ourselves mentally now for the next market fall. We can have the best laid plan and asset allocation in the world, everything neat and tidy down on paper.

But if we haven’t steeled ourselves in advance for the next shock, knowing that this is a question of “when?” rather than “if?” then it may all be for nothing.

By setting our expectations lower and by being realistic, we maximise our chances of behaving sensibly when our situation most demands it. That is, and remains, our primary job.

Past performance is not indicative of future returns. None of the above is intended to constitute advice to any individual. If you have any questions specific to your individual situation, please consult with a regulated financial adviser.

Comments